Book Summary of Cashflow Quadrant by Robert Kiyosaki

Introduction - Book Summary of Cashflow Quadrant

Take Your First Step Towards Financial Freedom

Have you ever fantasized about giving your notice to your boss, leaving the grind behind, and leading a prosperous life? You’re not by yourself. But for many of us, those aspirations will always be only that—aspirations.

Robert Kiyosaki took that common fantasy and turned it into the wealth and freedom he enjoys today. His own father had been an overworked government employee who had gone bankrupt and racked up debt. Kiyosaki made a promise to himself that he would never let that happen to him. So he discovered how to make money wherever he was.

Kiyosaki has spent decades building profitable businesses and investment portfolios. You’ll learn the overarching concepts that have guided him throughout his achievement rather than specific approaches.

You’ll discover:

- The four different types of cash flow

- The implications of the information age for our employment and retirement benefits

- How fear affects how we see financial matters.

Book Summary of Cashflow Quadrant Main Idea 1

Hard Work Alone Won't Bring Financial Security

Robert Kiyosaki had two father figures during his childhood in Hawaii. One was his government-employed biological father. The other was the self-made businessman and investor father of his friend Mike.

These are his Rich Dad and his Poor Dad. Kiyosaki’s biological father appeared to be successful on the outside; he was intelligent and well-liked. He had achieved the position of Head of Education in the Hawaiian government after excelling academically. But because he worked for the government, he was overworked and often on the road. His calendar was full of appointments. He consequently had little free time to appreciate his second interest of reading books or to spend time with his family.

He also had little money although playing a coveted government position. Even though he was a wise and well-traveled man, he continued to subscribe to the dominant myth of the day, which holds that achieving financial security via hard effort alone is possible. This was a result of his subpar financial education, despite having a superb academic education. In fact, he openly made fun of anyone who took real estate or investing programs since he didn’t believe there was such a thing as a financial education.

Mike’s father, the entrepreneur and investor, on the other hand, always appeared to have both time and money. He seemed to spend more time with the author than his biological father did, in fact. He had long ago made the decision to attempt to avoid the drudgery of the 9 to 5 and become a business owner and investor instead of an employee. He started buying real estate early in life, little by little. He eventually created a hotel empire and was instrumental in the development of Wakiki Beach.

Book Summary of Cashflow Quadrant Main Idea 2

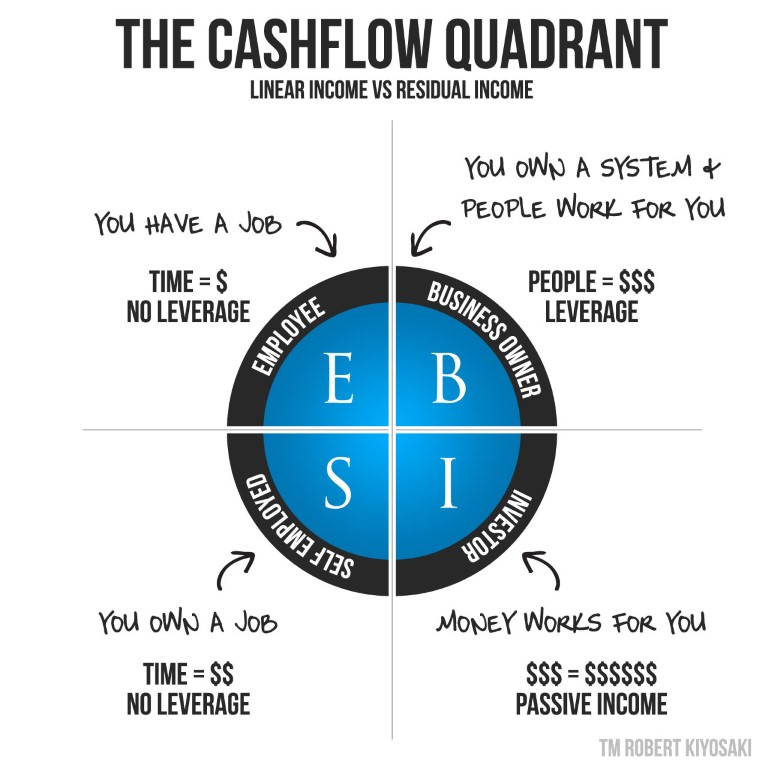

People Fall Into One of 4 Cashflow Quadrants

There are four quadrants in which we might categorize the various ways we make money.

E, S, B, and I are the letters used to identify each of them.

The letters E and S stand for “employee” and “small business or self-employed,”.

The B and I stand for “large business owner” and “investors,”.

Now, you fall into one of these four quadrants based on how you earn a living.

You might make money from just one, a few, or all of these quadrants during the course of your lifetime. Consider a doctor practicing medicine in the United States today. He could choose to become an E to support himself (an employee). He can do that by working for the government in public health, becoming a military physician, or joining the staff of a sizable hospital or insurance provider. In other words, by accepting a 9 to 5 job.

The same doctor also has the option of opening a private practice as a S (self-employed). He would open an office, appoint staff, and compile a patient list in confidence. He would have greater control, but it’s still laborious work.

The doctor’s third choice would be to decide to become a B. (big business owner). He might run her own clinic and employ medical professionals. In that situation, he would probably hire a business manager to run the company. He wouldn’t have to work in the clinic even though he would own it. He may, however, continue to practice medicine and run a non-medical company at the same time.

He would undoubtedly have investable income as he was a highly-paid doctor. He might therefore continue to practice medicine, manage his clinic, or manage his business while also becoming an I (investor). He could do that by making investments in stocks or real estate.

So far, so easy, am I right? This is how our society is fundamentally structured. These four quadrants each call for a unique set of skills and personality traits. There is no “right” or “wrong” decision for some people; they find their place in life and are content no matter which quadrant they choose to live in.

But what if you seek financial independence?

What if you wish to get away from the grind of the workplace?

In that case, you’ll need to transition from the E and S to the B and I quadrants.

In other words, going from working to owning.

Book Summary of Cashflow Quadrant Main Idea 3

You Must Take Responsibility For Your Financial Situation

We currently reside in a period known as the “Information Age.” It started around 1991. The “Industrial Age” came to an end as a result of new technologies that made it possible for businesses to send money across the globe at breakneck speeds.

Additionally, it marked the beginning of the end for stable, unionized employment and respectable public pensions. But a lot of us are still struggling to change with the times. We cannot rely on the government to protect us in the current economic climate. We must take responsibility for our own financial stability.

In fact, a lot of us still have a tendency to think like our grandparents did. That is, we anticipate that the government will look out for us in later life if we work hard and pay our taxes. Sadly, today’s world makes this kind of arrangement impossible.

For instance, it is predicted that more than 150 million Americans will be looking for government assistance in 2030. These will include government workers, veterans, teachers, other public servants, and retirees looking forward to receiving Social Security and Medicare benefits. They have every right to anticipate assistance because they contributed to the system and were promised something in return.

It appears unlikely that these assurances will be fully kept, though. Simply put, the price is too high. Additionally, the ultra-rich will simply relocate to nations with lower tax rates if the government increases taxes to pay for these promises.

Therefore, it is false to believe that if you work hard, the government will take care of you. What then ought to you do? You’d better move into one of the right-hand quadrants, B or I: Big business ownership or Investment, if you want to enjoy financial security for the rest of your life.

Again, Kiyosaki learned a crucial lesson from his two father figures’ experiences. His biological father put a lot of effort into his job as a government employee and anticipated financial security. He lost his job as a result of a political disagreement, and the Hawaiian government blacklisted him. He was devastated. He tried a few business ventures but failed because he lacked experience in the B and I quadrants. As a result, he became heavily in debt. He bitterly realized that nothing would be there to catch him as he fell.

But Kiyosaki’s “rich dad” had established a system of passive income, a steady stream of money flowing into his bank account. Early in life, he moved into the I quadrant, which protected him for the rest of his life.

Book Summary of Cashflow Quadrant Main Idea 4

Working Hard and Working Smart Are Two Different Things

The author was staying at Mike’s house one day when his “rich dad” sat him down and told him a tale. It marked a significant turning point in his financial education.

This story would clarify the key distinction between those in the E and S quadrants and those in the B and I quadrants. Once upon a time, a charming little village existed. The lack of a water supply was the only issue. The village elders decided to hire two men, Bob and Ben, to fix this.

Bob, the first contractor, got to work right away. He made the choice to carry two steel buckets to a nearby lake, fill them, and then return with them. He had to fill the water tank himself, which took him hours. He was worn out by the end of the day. However, he was at least getting paid for his work.

Ben, the other contractor, temporarily disappeared, which pleased Bob because it eliminated his competition. But Ben didn’t do nothing. Ben had written a business plan, established a corporation, located investors, hired a president, and gathered a construction crew in place of purchasing two steel buckets to transport the water.

A stainless steel pipeline linking the village to the lake was constructed by Ben’s team in less than a year. Ben quickly added more villages to his pipeline after that. Compared to Bob’s, his water was better, more affordable, and more accessible. He quickly started to profit from the entire system he had built. He soon had absolutely no work to do. Poor Bob, on the other hand, was striving to make ends meet at any cost.

Ben eventually sold his pipeline company and retired in great wealth. Bob, however, was powerless to stop his children from abandoning his water-bucket business and moving away to the city.

This is the difference between the left and right hand quadrants—working hard and working smart.

Book Summary of Cashflow Quadrant Main Idea 5

Different Quadrants Require Different Mindsets

Let’s start by taking a look at the E quadrant. These are the people who work for companies. Those who are drawn to this quadrant frequently use phrases like “security” and “benefits.” They require a sense of security, which can come from a contract, a consistent paycheck, and benefits from their job. They are frequently motivated by fear, particularly fear of risk and financial ruin. Employees can range from janitors to company presidents. They are defined by the contractual security they have chosen, not by what they do.

The S quadrant is the second. They are independent contractors or small business owners. These individuals enjoy being “their own boss.” They don’t like having their income set by others when it comes to money; if they work hard, they expect to be paid well. In contrast, they are aware that if they don’t do a good job, they will be paid less. They tend to be perfectionists who think they are the only ones capable of performing at the highest level. Independence is more valuable to them than money. Additionally, they are motivated by fear, specifically the fear of losing their independence.

The B quadrant, which includes large business owners, is the third segment. They differ significantly from those in the S quadrant in many ways. They enjoy surrounding themselves with intelligent individuals from all the other categories. Delegation is their strongest skill. A prime example is Henry Ford. Although he wasn’t the most skilled mechanical engineer or financial analyst, he was quite good at finding others to do those jobs for him. Those that are in the B quadrant have the option of leaving their entire business operating while they do nothing. Instead, they are in charge of a system that keeps bringing in money for them.

We now reach the I quadrant, which represents the investors. Frequently, the ultra-rich inhabit this area. Their capacity to take calculated risks is what distinguishes them. They don’t mind volatility like gamblers do. It’s no longer as risky a proposition because, unlike gamblers, they enjoy researching their risk. A great investor like Warren Buffet is able to accept the risk of a turbulent financial environment while also making sure to fully comprehend the associated hazards. This is the essential quality for everybody who wishes to achieve financial independence.

Book Summary of Cashflow Quadrant Main Idea 6

Starting Your Own Business and Investing Is The Way

Most wealthy people started off in the B quadrant before moving to the I quadrant. The cause is fairly obvious. Accumulating wealth is essential for becoming wealthy. The safest method to do it is to invest in stocks, ETFs, or real estate.

But you’ll need a ready flow of money and time to invest wisely. The greatest way to do so is to launch a business that can generate income while you’re asleep. This entails creating a comprehensive system that can function without you, much like Kiyosaki’s “wealthy dad” and his hotel business.

Your investment options are constrained if you don’t have that available funds. However, if you invest huge quantities of money wisely, you can transition from the financial stability of business ownership to actual financial independence.

There is still another solid reason to take this route. You’ll be well-prepared to become a great investor if you can succeed in business. You’ll instinctively know which business ideas will produce greater, more durable investment returns.

Without this business sense, you can be putting yourself up for a loss on your investment. Many people in the E and S quadrants make hasty attempts to enter the I quadrant, but since they lack knowledge of what constitutes a successful business system, they make poor investments. They won’t have much money to invest as they don’t have a big organization of their own. Their investment risk is increased as a result.

Investors can be categorized into five different groups.

- Finance Intelligence Level 0 Unfortunately, this describes most of us. These are the people who, although being temporarily wealthy, have nothing to invest. This happens because people accumulate more debt than their salary can support. They need to first balance their fundamental finances before they can start investing.

- Losers-Are-Savers Level. As the name implies, this level is also financially illiterate. The conventional wisdom has long held that merely saving money will ensure future financial security. The modern economy has relatively low interest rates, therefore there is very little return if you simply leave your money in a bank account. And as we seen during the financial crisis of 2008, people who had invested their money in bonds—that is, in government loans bundled into retirement funds—often had their investments completely destroyed. Saving is not enough.

- Too-Busy-Investor. These are the people who just pass their money over to a financial advisor. Despite the fact that these investors frequently have greater success than the first two groups, they nonetheless take a big risk. Many people discovered after the 2008 financial crisis that their “trusted expert” was anything but, and they lost a sizable portion of their investment. This is a result of the fact that they trusted individuals with their money who weren’t themselves successful investors. Instead, they were only staff members at advisory firms.

- Professional Grade The first genuine investor kind is this one. These are the individuals who educate themselves on various forms of investment, such as real estate or stocks. They also conduct their own in-depth research. They become more focused on their assets as a result, and they get a solid financial education that will benefit them throughout their life. No matter what else we accomplish, it would be wise for us all to achieve this degree of understanding in our unstable environment. A good investment in itself is receiving a financial education.

- Business Level. This is Warren Buffett territory. Two steps are involved. You must first succeed as an entrepreneur or successful B. After that, you invest your money in risky projects. The steepest mountain to climb is also the best path to tremendous riches. The investor level “I’m-A-Professional” is more doable if creating a business empire isn’t your goal!

Book Summary of Cashflow Quadrant Main Idea 7

Think Long Term But Start Today

There are many of us who have irrational anxieties about a variety of topics, including money. Deep fears about money can arise. Since money is so important to our well-being, many people find it difficult to think rationally about it. Instead, they tend to feel emotionally while discussing it. Just keep an eye on how the financial markets function. They don’t even move “rationally,” but rather wildly, leaping and falling because of fear and greed.

However, when it comes to money, it’s crucial that logic prevails over these emotions. In actuality, investing in real estate or the stock market doesn’t have to be so scary and risky. The rules are actually extremely easy to understand, just like in the board game Monopoly.

“A journey of a thousand miles begins with a small step”.

You should be cautious about trying to become wealthy quickly. Get Rich Quick schemes, those countless courses and publications that guarantee instant success, are all around us these days. A lot of them sound fantastic. But in truth, the only person who will profit from them is the seller.

We frequently seek out instant gratification. Everything appears to be designed to help us achieve our goals as quickly as possible. However, as the proverb says, Rome wasn’t built in a day. Consequently, you must start small and make doable goals. Don’t push yourself or your finances too far in your haste to become wealthy.

Additionally, planning for the long term entails adopting a practical mindset. Sadly, job security will be reduced in the future because the Information Age is expected to be extremely turbulent. Don’t become dependent on making money this way, even if you now have a beautiful work with a good salary. It’s not likely to continue forever.

In light of this, making long-term, compound investments is the greatest method for you to achieve financial independence. How do compound investments work? It entails starting small-scale investments right away and reinvested income or profits in your portfolio. Your profits will increase because your investment has increased. Your profits eventually increase steadily. “Compound interest is the eighth wonder of the world,” Albert Einstein once said.

You should spend money on your financial education in addition to other things if you want to be financially free. Your long-term safety may depend on it just as much. More helpful than a risky investment portfolio can be a solid understanding of the stock market or the real estate industry. You’ll then be equipped to resume your path to financial freedom, even if the future proves to be difficult.

Final analysis

There are four different ways to make money:

- As an employee.

- As a self-employed person or owner of a small business.

- As a huge business owner.

- As an investor.

Move away from the first two and become a business owner and investor to gain true wealth.